Gifts of Life Insurance: Getting Started

Life insurance is an asset you may not think of donating to Easterseals Midwest until you hear how powerful, practical and simple it can be.

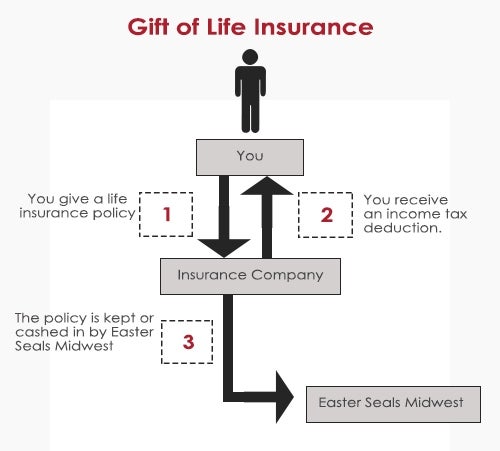

How It Works

When you own a life insurance policy with accumulated cash value, you're essentially sitting on a pile of money. When the original purpose for the protection no longer applies—such as to educate children now grown or to provide financial security for a spouse now deceased—your life insurance can be redirected to help support a worthwhile cause. One option is simply to name Easter Seals Midwest as the primary beneficiary. (Naming us as beneficiary while you retain ownership of the policy, however, does not qualify you for an income tax deduction.) Or, you can name us as the beneficiary and also assign us ownership of the policy as a current charitable gift. Doing so provides you tax benefits as outlined below.

How You Benefit

When you assign us ownership of a life insurance policy and also name us as the beneficiary, the following good things happen:

- You receive an income tax charitable deduction, available under most circumstances.

- You realize tax savings from use of the deduction, and these savings can be invested for future income.

- You reduce your future estate tax liability.

Donating a New Policy

Perhaps you don't own an existing policy but still realize how beneficial giving life insurance can be. If so, you can—in most states—purchase a new insurance policy and name a qualified charity like ours as the beneficiary and owner of the policy. Rather than paying premiums to the insurance company, you make tax-deductible cash gifts to cover the annual premiums. Even greater leverage is possible when two donors, usually spouses, purchase a two-life second-to-die policy. With two lifetimes before the payment of death benefits, a future gift to us will cost you even less.

But What About the Kids?

You want to make a significant gift to Easterseals Midwest but not at the expense of the kids. Is it possible to do both? As a matter of fact, yes—with life insurance.

How It Works

If making a donation to Easterseals Midwest threatens to reduce the amount you can leave to your loved ones, life insurance can make up the difference. Depending on your age, health and marginal income tax rate, the money you save in taxes thanks to the charitable deduction you will receive for your donation can be used to purchase life insurance with death benefits equal to the value of your gift.

Another Option

Rather than owning the new life insurance yourself, it may be preferable to own the policy inside an irrevocable life insurance trust (also called a wealth replacement trust). You would typically name a bank trust department or trust institution as trustee. Doing so will enable your heirs to receive the death benefit of the life insurance without having to pay estate taxes. Plus, life insurance is generally income tax–free to your beneficiaries.